PDF Format

Issue Contents Issue Contents

All Issues

Winter 2008

Volume 8, Number 2

The information in Tax Perspectives is prepared for general interest only. Every effort has been made to ensure that the contents are accurate. However, professional advice should always be obtained before acting and TSG member firms cannot assume any liability for persons who act on the basis of information contained herein without professional advice.

Taking Advantage of Low Values, How About an Estate Freeze

By Kim Moody, CA, TEP

Moodys LLP Tax Advisors (Calgary)

Given our current economic environment, the time to consider an estate freeze may never be better.

Many businesses and most industry segments have recently realized a significant reduction in value. If one believes that this is temporary and valuations will rebound in the future, consideration should be given to whether it is now the right time to carry out an estate freeze.

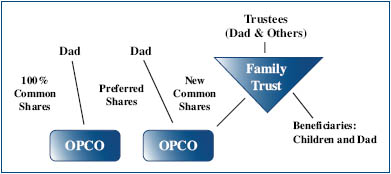

As many readers know, an estate freeze can be very useful when planning for the succession of a family business run as a private corporation. In a typical estate freeze, the shares of a private corporation (Opco) may be owned by Dad. Suppose Dad is age 65 or thereabouts and wants to gradually transition the business to his children. After carefully planning the succession, the estate freeze can be accomplished by having Dad exchange, on a tax-deferred basis, his common shares of Opco for a class of shares that are frozen in value. Such shares would be preferred shares with a redemption value equal to the value of Dads common shares. The children would then purchase new common shares, possibly via a family trust. Through this, the future growth of the business will go to the next generation.

If the redemption value of Dads preferred shares is higher or lower than the current value of Opco, negative tax consequences can arise to Dad. Therefore a reasonable attempt to value Opco must be made, and a price adjustment mechanism should be included in the bundle of rights of the preferred shares and/or transfer agreement.

Upon Dads passing, his estate will deal with the preferred shares by either transferring them on a tax-deferred basis to his surviving spouse or distributing them to children in conjunction with his well-thought-out estate plan. If the shares are transferred to his children and not to his surviving spouse, then capital gains tax will arise at that time. Given this tax consequence, it is usually desirable to ensure that the redemption value of the preferred shares is as low as possible hence the interest in carrying out an estate freeze now.

Dad does not need to wait until death to realize the value of the preferred shares. Given that the tax rate on dividends has declined in recent years, it may make sense for Dad to receive remuneration in the form of dividends from Opco by having Opco repurchase some of his preferred shares over time. The repurchase results in a dividend to Dad which, depending on Opcos situation, can be treated as either an eligible dividend (subject to preferred taxation rates) or as a non-eligible dividend. With careful planning, the preferred shares can be redeemed entirely over a number of years, thereby eliminating the ultimate tax implications upon Dads passing.

Suppose Dad is concerned about having enough money for retirement and/or having control of the family business. Both matters can be resolved by using a family trust under which Dad is a beneficiary and possibly a trustee. Also, Dad can be issued special voting shares to control Opco into the future.

Given the current situation, Dad will eventually pay capital gains tax upon passing the business to the next generation. The prudent estate plan will always look for opportunities to freeze an estate to the extent desirable when current valuations are low so as to minimize the eventual tax consequences upon Dads passing. Given the current economic environment, is today the right time to consider such planning? Logically, for certain situations, the answer should be, Yes!.

|